As the US presidential election race grinds onward, the issue of the nation’s healthcare system—or, rather, the lack of it—has been getting some airplay. I recently saw a video of people in the UK being asked what they think health care actually costs in the States. Everyone was deeply shocked and horrified that such a system could actually exist in the 21stcentury. I’m here to say: it’s all true. I’ve written elsewhere about America’s approach to healthcare. Today, let’s take a journey through the maze of private insurance in America. Be prepared to add up some significant costs.

Copays and Coverage

First, the issue of private insurance and what it does and doesn’t cover. Three months ago, on a trip back to the UK, I was bemoaning the costs of medicines to a British friend, pointing out the high monthly cost of insulin. She was staggered. “What? A life-saving medicine and you have to pay for it? I thought you had insurance?!” We do; but just because something is insured doesn’t mean you get it for free.

Private insurance comes with a job—not every job, especially not if you work part-time work or for a small company. Larger companies and the private sector usually offer some kind of plan; unless you work for a low-paying service sector company like Walmart, many of whose employees are encouraged to get Medicaid. The scores of different insurance companies each offer many different plans, with different levels of coverage. It’s up to the company what they choose to offer; bearing in mind that the company will be paying a hefty chunk of change to offer any kind of plan to their employees. According to research by the Kaiser Family Foundation, the average cost to an employer for providing coverage for an employee’s family is now over $20,000 a year.

Now, to the first cost: almost all of the plans come with copays—meaning, the amount you have to fork over for prescriptions, doctor visits, procedures, etc. Our current insurance plan comes through Spouse’s work. There’s a $30 copay for every doctor or office visit. That doesn’t sound too bad, right? But then there’s prescription copays, which for us, under our current plan, vary widely from $1.25 for a one-month supply to (on one memorable occasion) north of $100.

That’s assuming your meds are covered. I still find it surreal to be discussing a problem and treatment options with the doctor, then have her stop and say, “Wait, what insurance do you have? They don’t all cover X.” It’s also often the case that the insurance may insist the doctor provide documentation proving that options A, B, and C have been tried and rejected before they will approve treatment X. Doctor’s offices have to waste inordinate amounts of time dealing with demand for documentation from multiple insurance companies.

It gets better. Each insurance plan also has a ‘formulary,’ a list of what meds they cover, at what level, and what they don’t. Every year, in November, the plans send out their information for the coming year, including how much your monthly premium will be (it always goes up, always) and any changes to the covered/excluded meds. Yes, that’s right, a medicine that was covered this year may not be covered next year because of some reason (usually financial) that makes sense to the insurance company, but not to you or your doctor.

Premiums and Deductibles

About those premiums—that’s the monthly cost for your insurance. Almost all employers that offer health care require premium sharing. That means that the insured has to pay some portion of the premium before even using the plan. A relatively new “innovation” is for the employer to pay for the insurance of the employee only, with the employee picking up some to all of the premium costs of insuring a spouse and any progeny. A sister-in-law used to be employed as a social worker for the county; she told me she never had to pay a monthly premium, one of the few perks of an otherwise low-paying public sector job.

The premium will depend on the plan your company offers, the state you live in, and a whole host of other factors. The Big Corporation I used to work for was headquartered in Chicago, where we lived for a while, which is in the state of Illinois. As a pretty big local employer, the company was able to offer decent health insurance for a family of four for a premium of about $300 a month. The premium can come straight out of your pay, pre-tax.

When I first started work in the early 1990s, we had a choice of 4 different plans with different levels of coverage and costs. Gradually, the number of options dwindled as the costs for even a Big Corporation became more extreme. By the time we moved to Pennsylvania, there was only a choice of two plans for Illinois-based employees; and for those in Pennsylvania, a state with only a handful of employees, there was only one plan on offer, take it or leave it. When I last worked for them, our monthly premium for 4 was about $700.

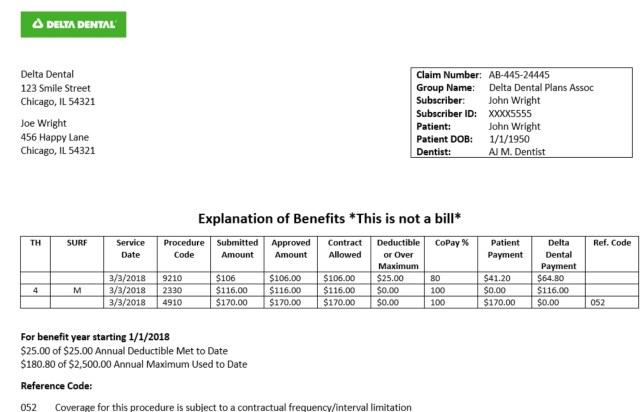

This is from the web–an example of the kind of statements you get from an insurance carrier, showing costs, coverage, copay, etc.

So, you’ve got copays and premiums to add up. But wait, there’s more! Meet, the annual deductible—that’s the amount you have to pay out of pocket every year BEFORE the insurance kicks in. Again, how much depends on the plan; it could be $500 for each family member and a total of $2,000 for the family as a whole, or even more. One little wrinkle is that if, for some reason, you change plans mid-year, the deductible for the new plan begins all over again, regardless of what you paid already under the old plan.

Employer Role

OK, so it’s a very expensive way to fund your healthcare costs; but at least private insurance gives you peace of mind, right? If only. Many of us, most of the time, don’t realize it but our healthcare options are dependent on the choices made by our employers. And sooner or later, that reality hits you, hard. Three years ago, the Big Corporation I’d worked at for 25 years told me, “We’ve reorganized the department and your role has been eliminated.” The family health insurance came with my job so, on top of everything else, we had to scramble to make sure we could switch to using Spouse’s firm’s health insurance, and also check to make sure it covered the various doctors and medicines we each used. Federal law says you can continue using your company health insurance for up to 18 months after leaving a job for whatever reason, but unless the employer provides a subsidy you have to pay the full premium yourself, i.e., both the employee cost and the company cost—which for us would have been well over $1,000 a month. Needless to say, we switched to Spouse’s coverage (and yes, had to meet a new annual deductible that year before the coverage kicked in).

Incidentally, you can only switch plans at the beginning of a new calendar year, making your choice in the November before the new year. The only exception that lets you change mid-year is if there’s been a “life-changing event,” like changing/losing a job, having a baby, or marrying.

A year ago, when Spouse’s firm merged with another one, the plan changed yet again, meaning we had to check whether our existing doctors, including a couple of specialists, would still be “in network.” Fortunately, they were, but if you have an unusual or particularly expensive condition, you may be stuck with some hefty costs. Paying “out of network” for a visit to a doctor can cost upwards of $150 as soon as you walk in the door. And, of course, we started again with a new annual deductible—in October.

Finally, the quality of insurance plans varies widely. I’ve mentioned the gradual reduction in choices at the Big Corporation over the 25 years I worked there. In the final couple of years, we were stuck with an 80:20 plan, i.e., after all the premiums, deductibles, etc. the plan only covered 80% of the costs of anything. For doctor visits that meant a co-pay of about $25 each time; but, had any of us needed any kind of procedure, especially something major like in-patient surgery, the cost would have reached well into four digits.

All Hail the Affordable Care Act

One of the many reasons I will always love former President Obama is the Affordable Care Act (ACA), the provisions of which were fully effective by 2014. Among other things, this stipulated that insurance companies could no longer deny coverage for existing conditions. Under this lovely little wrinkle, when you first attained new insurance the company would likely refuse to cover anything related to a pre-existing condition for the first year. This could be anything from high blood pressure and cholesterol meds and insulin, to pregnancy, and even cancer care. If not for the ACA, our two insurance company changes in the past three years could’ve cost us thousands of dollars.

And when I was laid off three years ago, what if we hadn’t had the option of switching to Spouse’s insurance? Neither of us is old enough to qualify for Medicare (federal senior health insurance which kicks in at age 65). So, I could have ‘bought’ my old insurance for a year; prayed I found a new job with benefits asap; spent our way into penury in order to qualify for Medicaid (health insurance for the poor); or, thanks to the ACA, we could have purchased a personal plan from one of the 20+ offered in the state of Pennsylvania. I looked into this briefly at the time, and quickly got overwhelmed at the number of options, with premiums that ran from $200 to $2,000 a month for a family of four, depending on family income, coverage, deductions, etc.

Meanwhile, Oldest Son is now 24. Thanks to the ACA, he has to be covered on our insurance until the day he turns 26. If, by then, he doesn’t have the kind of job that comes with health insurance (very possible given the field he works in), he’ll have to buy his own ACA plan.

Finally, everything I’ve talked about here has referenced basic private health insurance—none of which covers dental care and most of which do not cover vision care (unless it’s for something awful like an injury that is considered “medical”). So, in addition to the monthly premium for our family health insurance, which is about $450, we pay $116 a month in dental insurance (I have standard grew-up-in-Britain-in-the-1960s-and1970s teeth, they need a lot of help); and another $25 monthly for vision care (we all wear glasses and two of us use contact lenses, so everyone gets two vision checks a year).

A Surgery Story

Earlier this year I had surgery of the “do this now or eventually things will be much worse and potentially fatal” type. This necessitated multiple doctor visits ($30 each time), culminating in three hours in the surgical suite followed by two nights in the hospital. The process started with my regular doctor recommending a specialist who in turn recommended a surgeon—each time, I had to go home and check that these recommended doctors were in network. And each time, it took weeks to get an appointment as these specialists were in high demand. (So yes, there can be long wait times under Britain’s National Health Service, but the same is true here, too.)

(No, I wasn’t actually operated on by staff from Grey’s Anatomy!)

Eventually, I met with the surgeon who would be working on me (who, for the record, was absolutely wonderful). After she explained everything, I met with her admin staff to book the procedure. That person handed me many pieces of paper along the lines of “what to do/not do and what to expect” and one laying out the expected cost under our insurance: about $1,500. Had we not been able to afford that, there would have been no surgery, and I would be in increasing pain and getting steadily sicker.

After I was back home and recovering, the bills started to trickle in, listing the cost, the insurance payout, and the amount that we owed— sometimes things like the surgeon, the operating staff, the anesthesiologist, and the post-surgery nursing care are all on one bill, sometimes they bill separately. I do remember seeing the paperwork after Oldest Son was born and realizing that without insurance, our 36-hour delivery and stay would’ve cost about $10,000. That was 24 years ago; today, it would be closer to $30,000.

Missing the NHS

Back in 1992, I got one of those dreaded phone calls: “Mum’s in the hospital, it’s bad, you’d better come over.” Cue an emergency plane trip, and three harrowing days of discussing options with the doctors while holding the hand of a dying woman. The care Mum received was exemplary, the nurses unfailingly kind, and her death as dignified as was possible under the circumstances. And in all that crisis, there was one burden that never had to cross anyone’s minds: who was paying for all this?

So, when someone goes on a rant about how expensive a publicly funded health insurance scheme would be, how much people’s taxes would have to go up, and how much such a system “rations” healthcare, I tell them to take a step back. Add up how much you actually pay, out of pocket, for your healthcare—the premiums, deductibles, and co-pays. I’m pretty sure the tax cost would be less. And remember, too, that healthcare decisions in this country are made as much by the insurance companies as by the doctors.

I love this perspective – people try to claim that it’s as bad in other countries as it is here, and I know my British and Canadian friends always say that’s not true. Thank you for this – sharing it on my FB timeline.

LikeLike

Thank you, and welcome! I wrote this piece a year ago; in the middle of a raging pandemic with all the horrors that entails, it’s all become so much worse 😦

LikeLiked by 1 person